This report surveyed 161 DCWBC clients and 113 clients of 22 regional partner organizations, including the Latino Economic Development Center which translated it into Spanish and distributed it to their clients. Questions about the demography of business-owners, start date of the business, the type of business, its revenue and income, financing, and how it had responded to the COVID-19 pandemic were included. The survey of owners and entrepreneurs garnered data about their experiences running a small business before and during the COVID-19 pandemic. Following cleaning, deduplication and recoding, there were 274 unique responses.

Once all responses were collated and assessed, descriptive statistics were generated and analyzed. This primary data is compared and contrasted with other studies on women-owned businesses and also with data collected by the U.S. Census Bureau.

Results and Discussion

Quantitative Results

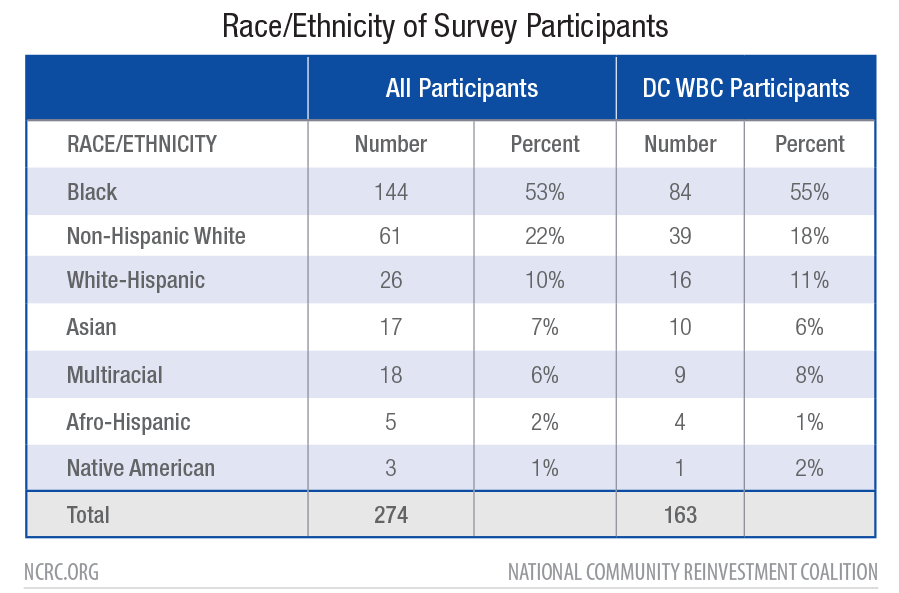

In all, 268 business-owners participated in the study, three of whom identified as male, three as non-binary, and the rest (267) as female. The participants in the survey were a diverse group of women entrepreneurs. The majority of participants were African-American at 53%, with Non-Hispanic White the next largest group at 22%, followed by White Hispanic at 10%, Asian at 7%, Multiracial at 6%, Afro-Hispanic 2%, and Native American 1% (Table 1). The client base of the DCWBC mirrored this demographic, with smaller proportions of Non-Hispanic White and Asian participants (18% and 6%), and higher of Black (55%), White Hispanic (11%), and Multiracial (8%) participants.

Table 1. Demographic composition of all participants in the survey, and of the DCWBC.

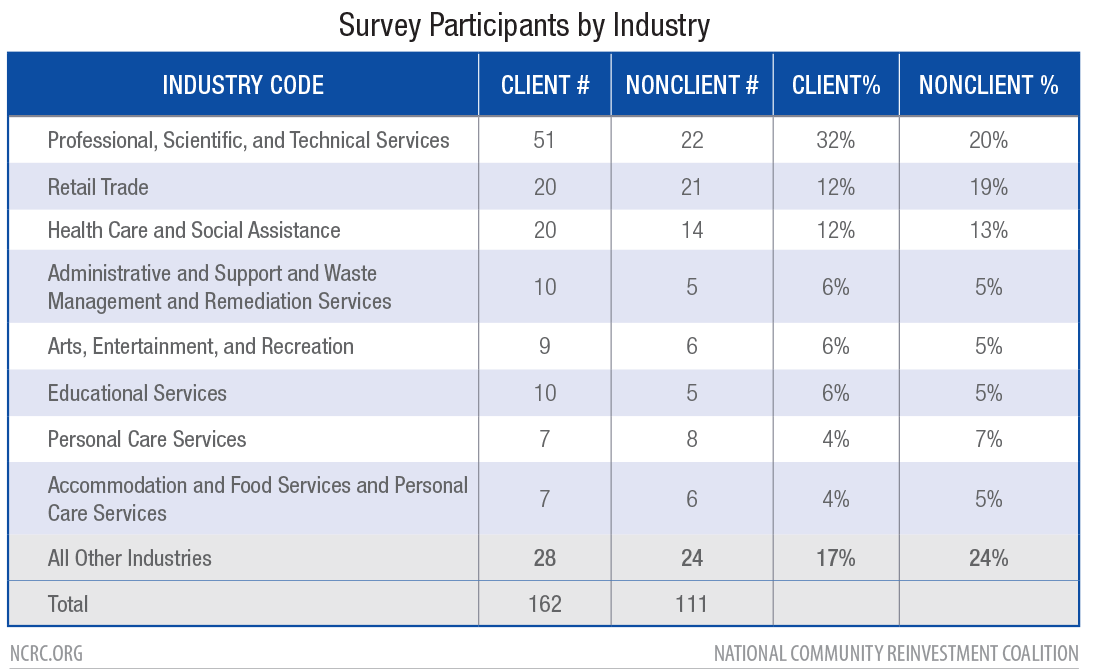

The small businesses included in the survey represented the full range of industries in the U.S., with women business-owners from 20 different types of industries and services participating. Table 2 reflects the primary category of industry in which 5% or more small businesses were engaged. The largest category, representing nearly a third of the businesses, is professional, scientific and technical services, followed by retail trade and healthcare and social assistance – which together constitute over half of the small businesses. Professional, scientific and technical services is a broad category including businesses engaged in legal services, accounting, architecture and design, computer programming, research, and advertising, and the participants reflected this wide variety of endeavors. Next, administrative support, arts and entertainment, educational services, personal care services, and accommodation and food services represent another quarter of the businesses. All in all, services-related businesses constituted almost 64%, while retail trade businesses were almost 21%, with the remainder engaged in manufacturing, construction, finance, information technology, or agriculture. The remainder of the participants (28 clients and 24 non-clients) were distributed across twelve additional industries, none of which had more than four businesses classified under a single code.

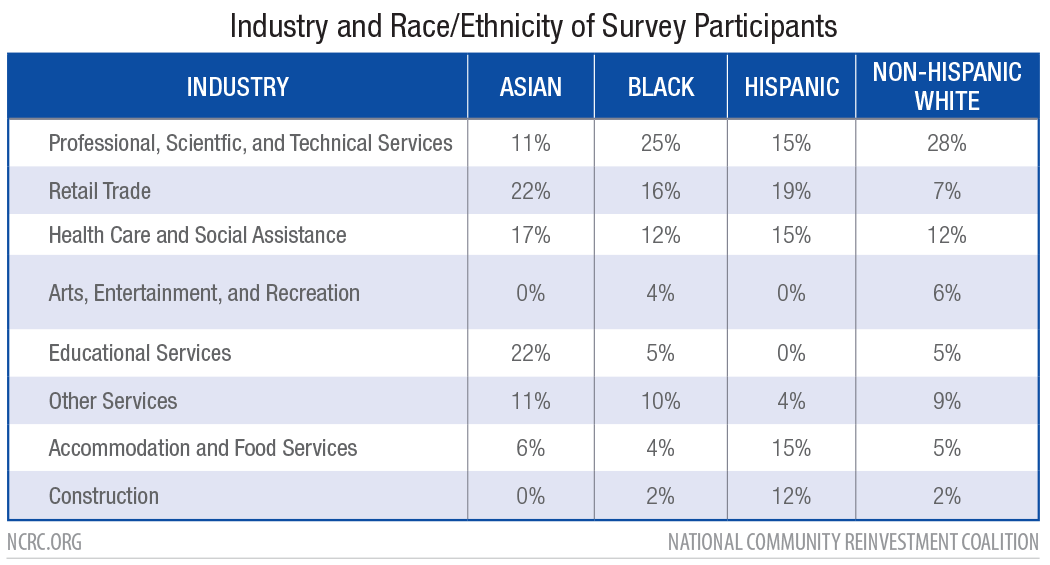

Table 2. Type of industries in which survey respondents are engaged. Codes derived from the North American Industrial Classification System. Industry codes for participants totalling at least 5% are included.

In terms of industry sector by race, the majority of White non-Hispanic and Black survey participants were engaged in professional, scientific and technical services (Table 3). The second most prominent category for Black entrepreneurs was retail trade, then health care and social assistance. For non-Hispanic White entrepreneurs, the second most numerous category is health care and social assistance. Hispanic business-owners were concentrated in retail trade, social assistance, professional services, and accommodation and food services. Asian entrepreneurs were mostly involved in retail trade and educational services.

Table 3. Industry composition as a percent of race/ethnicity of survey participants.

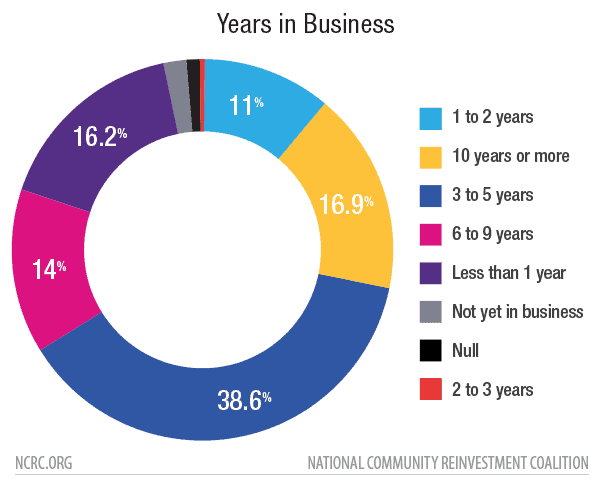

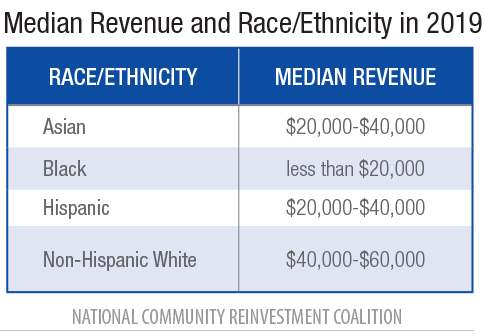

Disparities across racial and ethnic categories were evident in the revenue reported for 2019. Median revenue for Black-owned businesses was lowest—below $20,000 (Table 4), and a large percentage of Black women-owned businesses were also in this revenue category—49%, compared to 30%-33% of Asian, Hispanic and non-Hispanic White women-owned small businesses. The highest median revenue was reported by non-Hispanic White entrepreneurs—between $40,000 and $60,000. Both Hispanic and Asian business-owners reported median revenue levels between $20,000 and $40,000. The disparities between Black and non-Hispanic White businesses are partly explained by differences in the industries that these groups engage in. A higher percentage of non-Hispanic White women (28%) operated businesses in the professional, scientific and technical services than Black woman-owned businesses (25%). The professional, scientific and technical services industry category represents a broad spectrum of business types that vary considerably in revenue. Another explanation is tenure of business operations. Twenty-one percent of the Black woman-owned businesses in the survey had been open less than one year, compared to 15% of those that were non-Hispanic White woman-owned. Additionally, Black women-owned businesses open 10 or more years were 15% of survey respondents, while non-Hispanic White business owners with the same tenure were 21% of the total.

Table 4. Median revenue for 2019 by race/ethnicity of the business-owner.

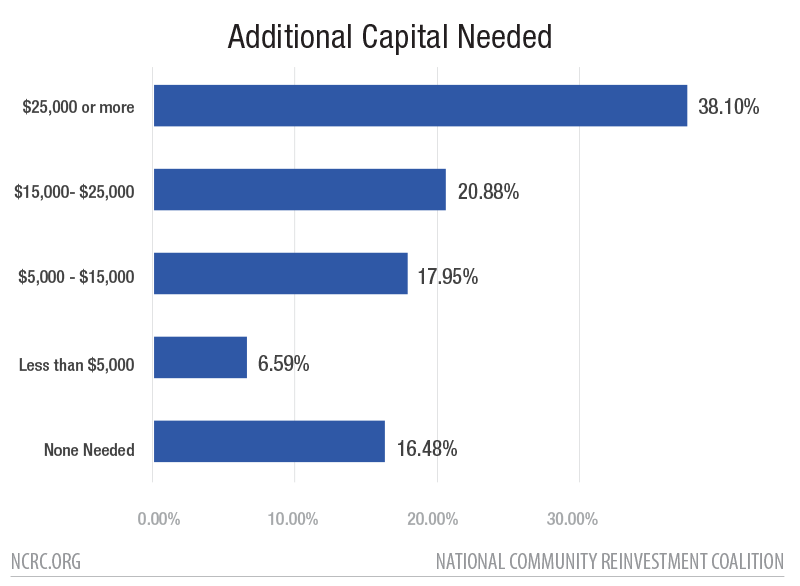

The participants were asked to specify their current need for capital (Figure 1). Only 16% of the businesses had adequate capital available and did not need further aid or investment. Businesses needing $25,000 or more were the largest group at 38% of respondents. The next were businesses needing $15,000 to $25,000, which was 21% of the survey. Businesses needing $5,000 to $15,000 were 18%, while the businesses needing less than $5,000 were only 7%. Businesses with higher revenue either had high capital needs, or did not need additional capital at all. Sixty-one percent of businesses with revenues over $100,000 needed an infusion of $25,000 or more, while 21% had no need for additional capital.

Figure 1. Capital needs of the survey respondents.

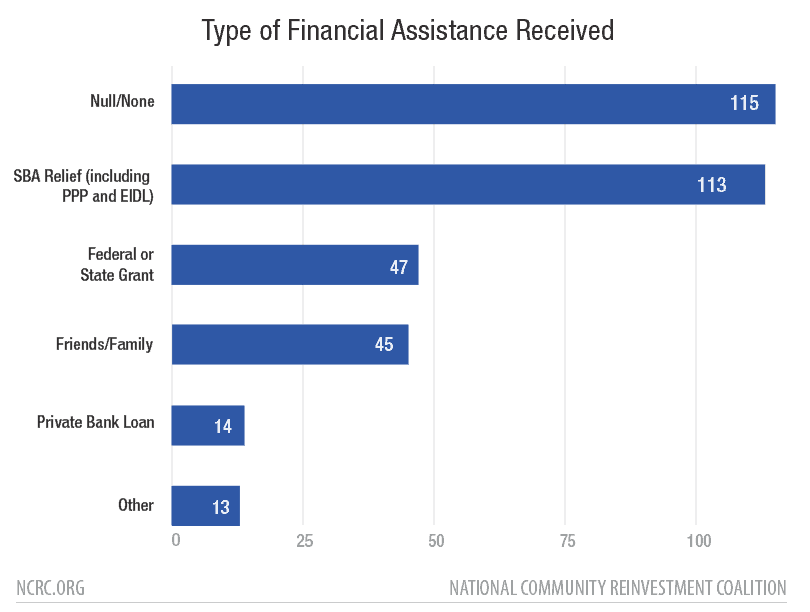

A high percentage, 42% of businesses, received no assistance from federal, state, local grants, from bank loans, or from friends and family during the pandemic (Figure 2). Of the businesses that received support, the SBA’s Paycheck Protection Program (PPP) and Economic Injury Disaster Loan (EIDl) were the most frequent programs cited, and 41% received this aid. This was followed by a smaller percentage of entrepreneurs receiving assistance from federal or state grants, friends and family and other sources which includes crowdfunding and online lenders.

Figure 2. Assistance received by women-owned businesses during the COVID-19 pandemic as of February 2021. The federal PPP and EIDL programs were still open as of the writing of this report.

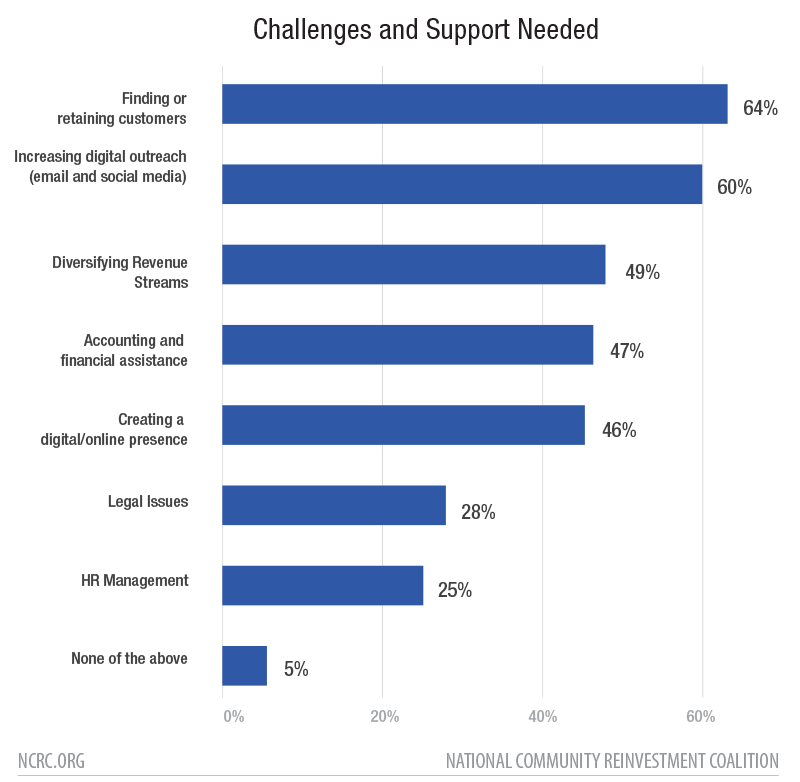

In terms of these small businesses needing assistance, over 60% of respondents wanted help finding and retaining customers – and associated with this, 60% wanted assistance expanding their digital outreach via social media or email (Figure 3). A further 45% wanted help establishing an online presence. This indicates that there is a strong need among the businesses for assistance with their digital marketing efforts. After that, diversifying revenue streams and help with accounting and financial assistance were cited as areas of need. This question in the survey was focused on areas in which the DCWBC might directly provide technical assistance to businesses, consequently funding was covered under different topic areas and was not a selection for the participants, which explains why capital acquisition was not a topic in this line of inquiry.

Figure 3. Challenges and assistance needed by businesses.

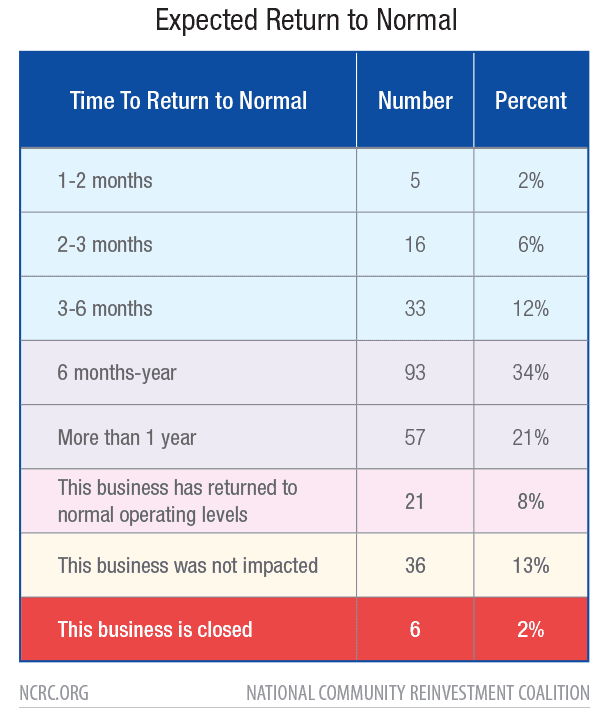

Finally, despite the difficulty operating a small business during the past year, business-owners remained, for the most part, optimistic about the future of their businesses and about the near-term resolution of the pandemic (Figure 4). Seventy-four percent believed that the pandemic will resolve this year, and 20% had already returned to pre-pandemic levels of operation. Thirteen percent were not impacted by the pandemic, of which 40% were in management companies and enterprises, and 29% in retail trade. It is probable that these had an online presence to make up for the difficulty of physical delivery of services. During the past year, social movements to “buy Black,” and others related to the Black Lives Matter movement, have been important drivers of change, and have asserted the importance of supporting the Black business community. All in all, only 2% of the participants in our survey had to close their businesses, though that may not be in line with overall experiences of women entrepreneurs, since the survey may have higher representation of active DCWBC clients who are currently receiving assistance from the center.

Table 5. Survey responses were collected from February 18, 2021, through March 16, 2021. This chart shows the pandemic impact on businesses with expected return to normal business operations expressed by survey participants.